[SMM Hot Topic] Steel Exports Pull Back Again, Where Will September Lead?

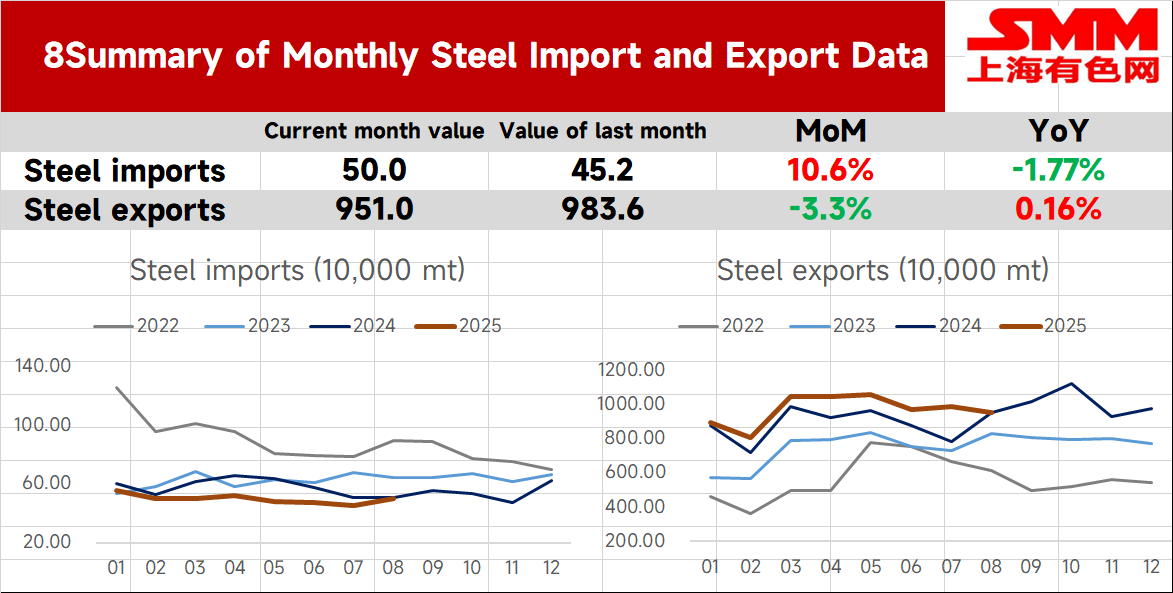

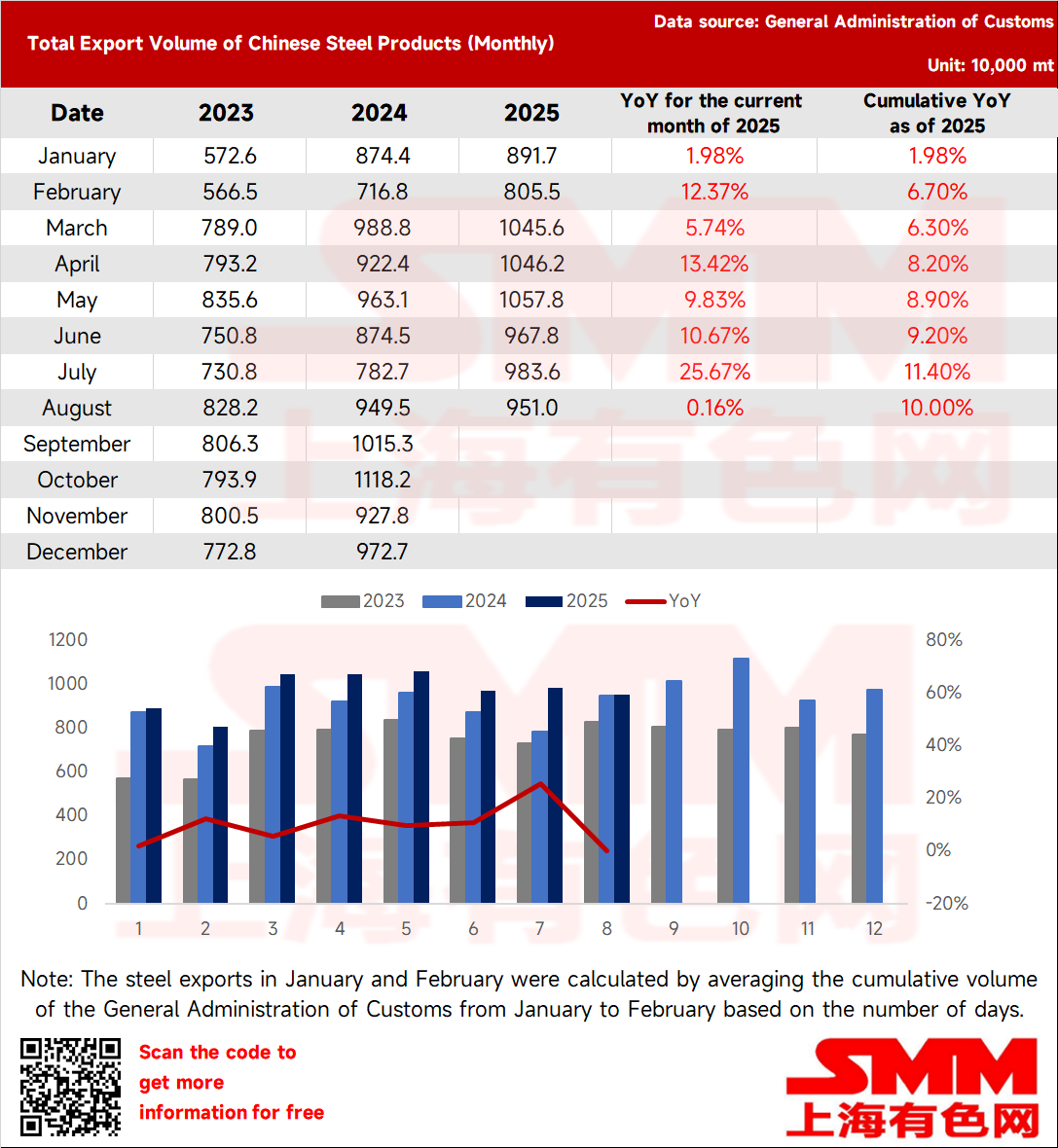

On September 8, data from the General Administration of Customs showed that China's steel exports in August 2025 reached 9.51 million mt, down 326,000 mt MoM, a decrease of 3.3% MoM. From January to August, cumulative steel exports totaled 77.49 million mt, up 10.0% YoY.

In August, China imported 500,000 mt of steel, up 48,000 mt MoM, an increase of 10.6% MoM. From January to August, cumulative steel imports stood at 3.977 million mt, down 14.1% YoY.

Overview of Steel Import and Export Data in August

- China's Steel Exports Edge Down

China's total steel exports in August fell 3.3% MoM. According to the SMM survey, domestic steel mills' HRC export plans in August amounted to 964,000 mt, compared with actual exports of 1.11 million mt in July, marking a 13.15% MoM decline. From July to August, domestic steel prices strengthened, prompting some mills to adjust overseas strategies, prioritizing domestic trade shipments, leading to reduced export orders. However, as new tax declaration rules will take effect from October 1, 2025, some MDs accelerated shipment schedules, limiting the overall MoM export decline.

- China's Steel Imports Rise MoM in August

In August, China imported 500,000 mt of steel, up 48,000 mt MoM, an increase of 10.6% MoM. From January to August, cumulative steel imports totaled 3.977 million mt, down 14.1% YoY.

- Short-Term Outlook for Steel Exports

According to the China Federation of Logistics & Purchasing, the global manufacturing PMI in August 2025 stood at 49.9%, up 0.6 percentage points MoM, nearing the 50 mark. The global manufacturing PMI rose MoM but remained below 50 for the sixth consecutive month, approaching the 50 mark this month, indicating that while global manufacturing has not shifted from its weak recovery trend, the recovery momentum strengthened MoM. Currently, the global economic recovery is progressing slowly amid fluctuations. Trade frictions and geopolitical conflicts continue to disrupt the global economy, yet countries worldwide are increasingly seeking new cooperation pathways and optimizing supply chains, demonstrating growing resilience in global economic recovery. According to China's manufacturing PMI data, the new export orders index in August stood at 49.5%, up 0.1 percentage points MoM, marking the third consecutive monthly increase, indicating a slight improvement in market demand.

World Steel Association data shows that global crude steel production across 70 reporting countries reached 150.1 million mt in July 2025, down 1.3% YoY. China's crude steel output was 79.66 million mt (down 4.0% YoY), while production in other regions totaled 70.44 million mt. On a cumulative YoY basis, only Africa and North America recorded increased crude steel production, while all other regions saw declines.

As of September 5, 2025, FOB export prices for HRC from India, Turkey, and CIS were $530/mt, $540/mt, and $480/mt respectively, compared to China's FOB quote of $478/mt. China's price differentials stood at $52/mt, $62/mt, and $2/mt against these markets, with MoM changes in export competitiveness at -27.78%, +111.11%, and +31.92% respectively.

Per SMM survey data, China's steel mills planned HRC exports for September reached 935,000 mt, up 11,000 mt (1.2% MoM) from August's actual exports. Improved production margins prompted pace adjustments, while recent customs scrutiny boosted order intake for some mills, driving the planned volume increase.

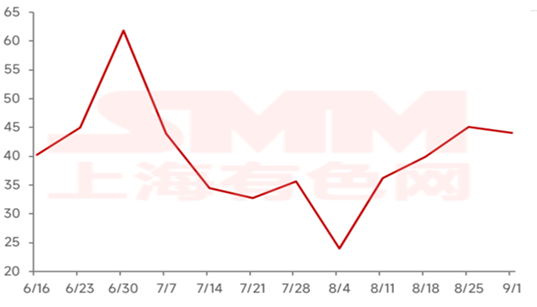

SMM shipping data indicates China's port departures totaled 12.04 million mt in August, up 6% MoM. August steel export orders rebounded significantly from July, attributable to enhanced price competitiveness for legitimate orders and traders' active pursuit of taxed orders for alternative products. The overall order intake remained moderate as export price advantages improved MoM. However, in terms of actual export performance, SMM expects steel product exports to pull back in September, primarily due to weak order-taking in July.

SMM Steel Product Export Orders (10,000 mt) - Excerpted from SMM Export Weekly Report

Copyright and Intellectual Property Statement:

This report is independently created or compiled by SMM Information & Technology Co., Ltd. (hereinafter referred to as "SMM"), and SMM legally enjoys complete copyright and related intellectual property rights.

The copyright, trademark rights, domain name rights, commercial data information property rights, and other related intellectual property rights of all content contained in this report (including but not limited to information, articles, data, charts, pictures, audio, video, logos, advertisements, trademarks, trade names, domain names, layout designs, etc.) are owned or held by SMM or its related right holders.

The above rights are strictly protected by relevant laws and regulations of the People's Republic of China, such as the Copyright Law of the People's Republic of China, the Trademark Law of the People's Republic of China, and the Anti-Unfair Competition Law of the People's Republic of China, as well as applicable international treaties.

Without prior written authorization from SMM, no institution or individual may:

1. Use all or part of this report in any form (including but not limited to reprinting, modifying, selling, transferring, displaying, translating, compiling, disseminating);

2. Disclose the content of this report to any third party;

3. License or authorize any third party to use the content of this report;

4. For any unauthorized use, SMM will legally pursue the legal responsibilities of the infringer, demanding that they bear legal responsibilities including but not limited to contractual breach liability, returning unjust enrichment, and compensating for direct and indirect economic losses.

Data Source Statement:

(Except for publicly available information, other data in this report are derived from publicly available information (including but not limited to industry news, seminars, exhibitions, corporate financial reports, brokerage reports, data from the National Bureau of Statistics, customs import and export data, various data published by major associations and institutions, etc.), market exchanges, and comprehensive analysis and reasonable inferences made by the research team based on SMM's internal database models. This information is for reference only and does not constitute decision-making advice.

SMM reserves the final interpretation right of the terms in this statement and the right to adjust and modify the content of the statement according to actual circumstances.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)